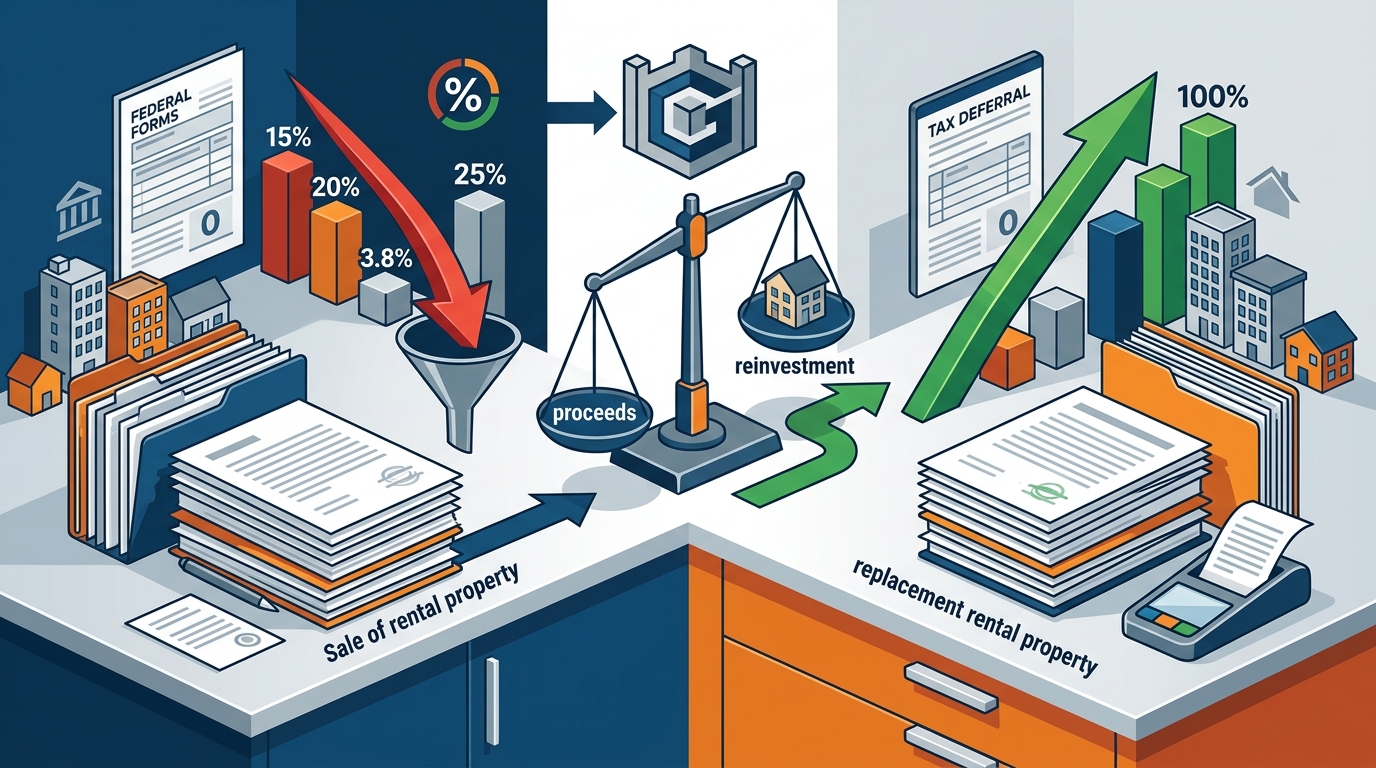

Selling a rental property can trigger a significant tax bill. Federal capital gains rates of 15% to 20%, plus the 3.8% net investment income tax and up to 25% depreciation recapture, can consume a large portion of your profit. A 1031 exchange lets you defer all of those taxes by reinvesting the proceeds into another like-kind investment property. This guide walks you through each step of the process so you can execute a compliant exchange with confidence, whether you own one rental or an entire portfolio.

What Is a 1031 Exchange?

A 1031 exchange is a transaction authorized by Section 1031 of the Internal Revenue Code that allows a real estate investor to sell an investment property and reinvest the proceeds into a like-kind replacement property while deferring capital gains taxes. The provision has been part of federal tax law since 1921 and, following the Tax Cuts and Jobs Act of 2017, applies exclusively to real property held for investment or business use.

A Qualified Intermediary (QI) is a neutral third party that holds exchange funds and prepares the documentation required for IRS compliance. Without a QI in place before closing, the IRS treats the sale as an ordinary taxable event.

Does Your Rental Property Qualify?

Most rental properties qualify for a 1031 exchange. The IRS requires that both the property you sell (the relinquished property) and the property you buy (the replacement property) are held for investment or productive use in a trade or business. Single-family rentals, duplexes, apartment complexes, commercial buildings, and even raw land all meet the like-kind definition under IRS regulations.

What Does Not Qualify

Properties held primarily for resale, such as fix-and-flip projects, do not qualify. Neither do primary residences or vacation homes used mainly for personal enjoyment. If a vacation property doubles as a rental, it may qualify under the safe harbor in Revenue Procedure 2008-16, but strict personal-use limits apply.

Step-by-Step Process for a Rental Property 1031 Exchange

1. Engage a Qualified Intermediary Before Closing

Your QI must be in place and exchange documents executed before the sale of your rental closes. This is not optional. If you take possession of the sale proceeds, even briefly, the exchange is disqualified. An independent QI like Granite Exchange Services prepares all exchange documents, holds funds in FDIC-insured segregated accounts, and coordinates with your escrow and title companies.

2. Sell Your Relinquished Property

Once the sale closes, your QI receives and safeguards the net proceeds. You never touch the funds directly. The 45-day identification clock and the 180-day exchange clock both start on the closing date.

3. Identify Replacement Property Within 45 Days

Provide your QI with a written, signed list of potential replacement properties before midnight on the 45th day. Use a legal description or street address to create an unambiguous identification. Granite Exchange Services provides deadline tracking and timeline calculator tools to help you stay on schedule.

4. Acquire Replacement Property Within 180 Days

Close on at least one identified replacement property within 180 calendar days of the relinquished property sale. Your QI wires the exchange funds directly to the closing agent. Upon completion, your QI issues a final exchange summary for your records.

5. Report the Exchange on Form 8824

File IRS Form 8824 with your income tax return for the year in which the exchange occurred. This form details the properties exchanged, the timeline, and the gain deferred.

Critical IRS Deadlines

Missing either deadline disqualifies the entire exchange and triggers immediate capital gains taxation. The two periods run concurrently, meaning the 45 days are inside the 180-day window.

| Deadline | Duration | Starts | Consequence of Missing |

|---|---|---|---|

| Identification Period | 45 calendar days | Day of relinquished property closing | Exchange fails; gain is fully taxable |

| Exchange Period | 180 calendar days | Day of relinquished property closing | Exchange fails; gain is fully taxable |

In limited disaster situations the IRS may grant deadline extensions. For example, California taxpayers affected by qualifying events between late 2024 and early 2025 received extended identification and exchange periods.

Replacement Property Identification Rules

The IRS provides three methods for identifying replacement properties. Each method caps either the number or value of properties you can list.

| Rule | Description | Best For |

|---|---|---|

| Three-Property Rule | Identify up to 3 properties of any value | Most rental investors |

| 200% Rule | Identify unlimited properties if total FMV does not exceed 200% of the relinquished property value | Investors comparing several options |

| 95% Rule | Identify unlimited properties if you acquire at least 95% of identified value | Large portfolio exchanges |

The three-property rule is the most commonly used by rental property owners because it offers straightforward flexibility without value caps per property.

How to Avoid Taxable Boot

Boot is any non-like-kind value received in an exchange, typically cash or a reduction in mortgage debt. Boot is taxable in the year it is received. To defer 100% of your capital gain, reinvest all net sale proceeds into the replacement property and take on equal or greater debt. Even a small shortfall creates a taxable event.

For example, if you sell a rental for $500,000 with a $200,000 mortgage, you must acquire replacement property worth at least $500,000 and carry at least $200,000 in new debt. Your exchange counselor at Granite helps structure transactions to minimize or eliminate boot.

Key Takeaways

- A 1031 exchange lets rental property owners defer federal capital gains, depreciation recapture, and the 3.8% net investment income tax.

- Both the relinquished and replacement properties must be held for investment or business use to qualify.

- You must engage a Qualified Intermediary before the sale closes; touching the funds yourself disqualifies the exchange.

- The 45-day identification deadline and 180-day exchange deadline are strict, concurrent, and rarely extended.

- Use the three-property rule to identify up to three potential replacement properties of any value.

- Reinvest all proceeds and match or exceed your existing debt to avoid taxable boot.

- Report every exchange on IRS Form 8824 with your tax return for the year the exchange occurred.

Frequently Asked Questions

Can I exchange a single-family rental for a commercial building?

Yes. The IRS defines like-kind broadly for real property. You can exchange a single-family rental for an apartment complex, a commercial warehouse, raw land, or even a Delaware Statutory Trust (DST) interest, as long as both properties are held for investment or business use.

Do I need to use a Qualified Intermediary?

Yes. The investor cannot receive or control the sale proceeds at any point. A QI holds the funds and facilitates the transaction. If the investor touches the money, the IRS will consider the exchange invalid.

What happens if I miss the 45-day identification deadline?

The exchange fails completely. The sale proceeds become taxable, and you owe capital gains tax, depreciation recapture, and potentially the net investment income tax for that tax year.

Can I do a 1031 exchange across state lines?

Yes. IRC Section 1031 permits exchanging real property located anywhere in the United States. Many investors sell a property in one state and buy replacement property in another. Granite Exchange Services handles exchanges in all 50 states.

How long must I hold the replacement property?

There is no statutory minimum holding period, but most tax advisors recommend holding the replacement property for at least one to two years to demonstrate investment intent. Selling too quickly may cause the IRS to challenge your exchange.

Is a 1031 exchange still available in 2025 and 2026?

Yes. Section 1031 survived fully intact in the "One Big Beautiful Bill" signed into law on July 4, 2025. No new caps, phase-outs, or restrictions were imposed on like-kind exchanges.

What is Form 8824?

Form 8824 is the IRS form used to report like-kind exchanges. It details the properties involved, the exchange timeline, and the gain deferred. Your QI typically provides the data you need to complete this form.

Start Your 1031 Exchange With Granite Exchange Services

Granite Exchange Services is an independent, CES-certified Qualified Intermediary that has guided investors through over 20,000 exchanges since 2000. Unlike corporate QIs owned by title or lending companies, Granite provides direct access to a dedicated exchange counselor who manages your transaction from start to finish. Call 800-899-6959 or visit the contact page to start your exchange today.