Selling a rental property can trigger a combined federal and state tax bill exceeding 30% of your gain. A 1031 exchange is the most powerful legal tool available to defer that entire burden and keep your capital compounding in real estate. Whether you own a single-family rental, a duplex, or a small apartment building, the process follows the same IRS framework under Section 1031 of the Internal Revenue Code. In this guide, we walk you through every step, from engaging a qualified intermediary to closing on your replacement property, so you can execute a compliant exchange with confidence.

What Is a 1031 Exchange?

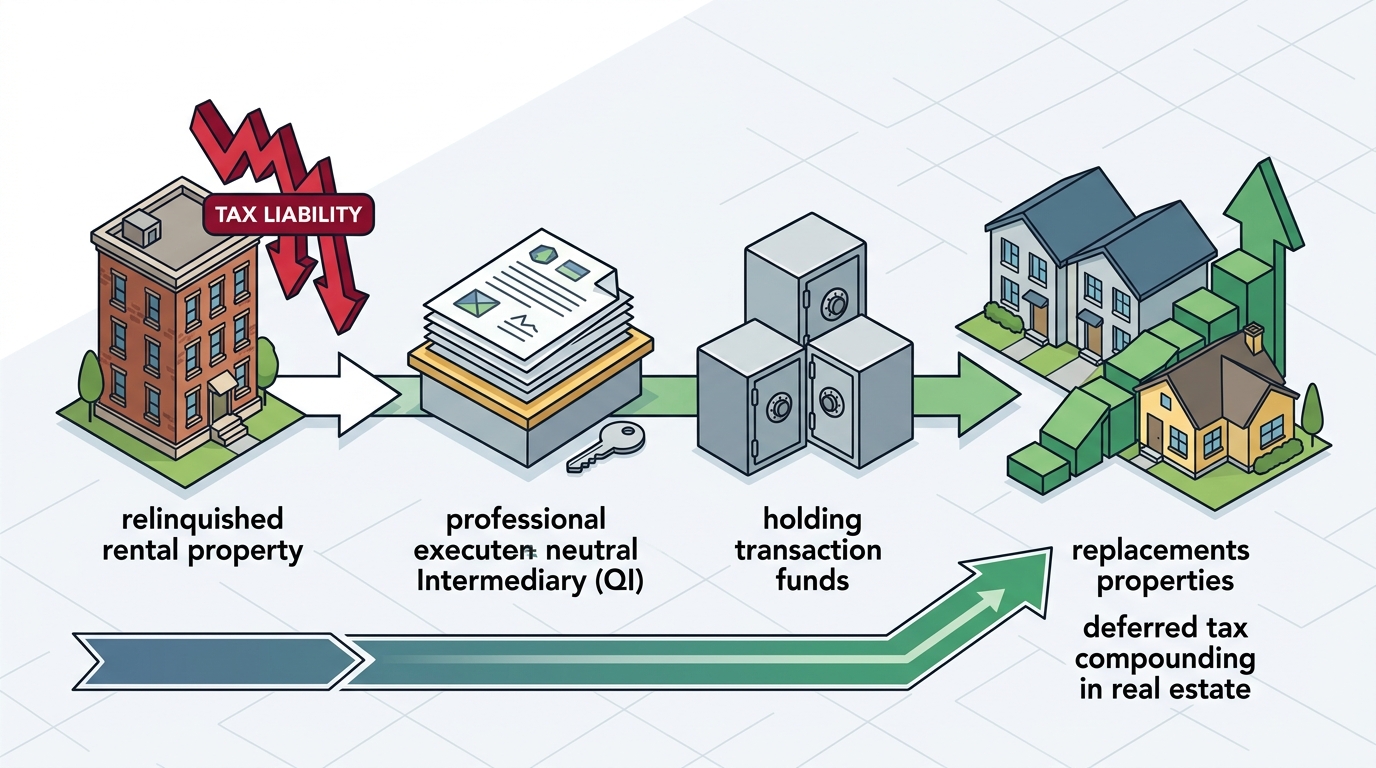

A 1031 exchange is a tax-deferral strategy authorized by IRC Section 1031 that lets you sell an investment property and reinvest the proceeds into a like-kind replacement property while deferring capital gains taxes. The term "like-kind" refers to the nature or character of the property, not its grade or quality. That means a single-family rental can be exchanged for a duplex, raw land, a shopping center, or even a Delaware Statutory Trust interest.

A qualified intermediary (QI) is an independent third party who holds sale proceeds and facilitates the exchange documentation so the investor never takes constructive receipt of the funds. Without a QI, the IRS considers the transaction a taxable sale.

Does Your Rental Property Qualify?

To qualify, both the property you sell (the relinquished property) and the property you buy (the replacement property) must be held for investment or productive use in a trade or business. Rental properties are one of the most common qualifying asset types. A property held primarily for resale, such as a fix-and-flip project, or a primary residence does not qualify. Review the full list of 1031 exchange qualifications before you begin.

Vacation Rentals: A Special Case

Vacation rentals can qualify under the IRS safe harbor in Revenue Procedure 2008-16 if they meet three conditions: at least 24 months of ownership, rental at fair market value for a minimum of 14 days per year in each of two qualifying periods, and personal use not exceeding the greater of 14 days or 10% of rental days. Properties used purely for personal enjoyment do not qualify.

Step-by-Step Process for a Rental Property 1031 Exchange

1. Engage a Qualified Intermediary Before Closing

Your QI must be in place before you close on the sale of your rental property. If sale proceeds touch your bank account at any point, the exchange fails. Granite Exchange Services sets up your exchange agreement, prepares assignment documents, and coordinates with escrow and title so funds flow directly into a segregated, FDIC-insured account. As an independent qualified intermediary since 2000, we are not owned by a title, escrow, or lender company, which means your interests always come first.

2. Close on the Sale of Your Rental Property

At closing, the net proceeds transfer directly to your QI. Your exchange is now officially open, and the IRS deadline clocks begin running.

3. Identify Replacement Property Within 45 Days

You have exactly 45 calendar days from the closing date to formally identify potential replacement properties in writing to your QI. The IRS allows three identification strategies: the three-property rule (any three properties regardless of value), the 200% rule (unlimited properties totaling no more than 200% of the relinquished property's value), or the 95% rule (unlimited properties if you acquire at least 95% of total identified value). Learn more about the 45-day identification rule.

4. Close on the Replacement Property Within 180 Days

You must acquire the replacement property within 180 calendar days of the original sale. These periods run concurrently with the 45-day window. Missing either deadline disqualifies the exchange entirely and triggers immediate tax liability. Our team tracks every date and sends proactive reminders so nothing slips. Understand the full 180-day exchange period requirements.

5. File IRS Form 8824

You must report the exchange on IRS Form 8824, Like-Kind Exchanges, and file it with your tax return for the year the exchange occurred. Your tax advisor handles preparation, but your QI provides the documentation needed to complete the form accurately.

Critical Deadlines You Cannot Miss

| Deadline | Days After Sale Closing | What Happens |

|---|---|---|

| Identification Period | 45 calendar days | Formally identify replacement properties in writing to your QI |

| Exchange Period | 180 calendar days | Complete acquisition of replacement property |

| QI Engagement | Before sale closing | Exchange agreement must be executed before close of escrow |

| Form 8824 Filing | Tax return due date | Report the exchange to the IRS with your annual return |

Both the 45-day and 180-day deadlines are strict and cannot be extended, even for weekends or holidays.

Exchange Structures for Rental Investors

Not every rental property transaction follows the same path. The right exchange structure depends on your timing, goals, and market conditions.

| Structure | How It Works | Best For |

|---|---|---|

| Delayed (Forward) Exchange | Sell first, then identify and buy replacement property | Most rental investors; the most common structure |

| Reverse Exchange | Buy replacement property before selling your rental | Competitive markets where you must lock in a property quickly |

| Improvement (Build-to-Suit) Exchange | Use exchange proceeds for construction or renovation on replacement property | Investors wanting to customize or develop replacement assets |

| DST Exchange | Exchange into passive fractional ownership in institutional real estate | Landlords seeking passive income without management duties |

Granite Exchange Services handles every structure listed above. Explore our full range of 1031 exchange services to find the right fit.

Common Mistakes That Disqualify an Exchange

Even experienced investors can stumble. Here are the errors we see most often:

- Taking possession of sale proceeds. If funds touch your account, the exchange is immediately invalid.

- Missing the 45-day identification window. There are no extensions or exceptions.

- Buying property of lesser value. Any proceeds not reinvested, known as "boot," become taxable. Boot is the portion of exchange proceeds that the investor receives as cash or non-like-kind property.

- Using a disqualified person as QI. Your agent, broker, attorney, or accountant who has worked for you in the past two years cannot serve as your intermediary.

- Exchanging into personal-use property. The replacement must be held for investment or business use, not as a primary residence.

Key Takeaways

- A 1031 exchange defers federal capital gains tax (15-20%), the 3.8% net investment income tax, 25% depreciation recapture, and applicable state taxes on your rental property sale.

- Your qualified intermediary must be engaged before you close on the sale. No exceptions.

- You have 45 days to identify and 180 days to close on replacement property. Both deadlines are absolute.

- Rental properties, including vacation rentals meeting IRS safe harbor rules, are among the most common qualifying assets.

- Like-kind is broadly defined: you can exchange a rental house for commercial property, raw land, or a DST interest.

- An independent QI protects your interests better than one owned by a title or escrow company with competing loyalties.

- The "One Big Beautiful Bill" signed July 4, 2025 left Section 1031 fully intact with no new caps or restrictions.

Frequently Asked Questions

Can I exchange a single-family rental for a commercial property?

Yes. The IRS defines like-kind broadly for real property. A single-family rental can be exchanged for commercial property, a multifamily building, raw land, or even a DST interest, as long as both properties are held for investment or business use.

What taxes does a 1031 exchange defer on a rental property?

A properly structured exchange defers federal long-term capital gains tax (15-20%), the 3.8% net investment income tax, 25% depreciation recapture, and any applicable state capital gains tax. On a $500,000 gain, that can easily exceed $150,000 in deferred taxes.

How long do I need to hold my rental before exchanging?

There is no statutory minimum holding period. However, holding the property for at least 12 to 24 months is generally recommended to demonstrate investment intent and avoid IRS scrutiny.

Can I do a 1031 exchange on a property I occasionally use personally?

Possibly. The IRS safe harbor under Revenue Procedure 2008-16 allows vacation rentals to qualify if rented at fair market value for at least 14 days per year and personal use does not exceed 14 days or 10% of rental days, over two qualifying years.

What happens if I miss the 45-day identification deadline?

The exchange fails completely. Your sale proceeds become taxable, and you owe capital gains tax for the year the property was sold. There are no extensions or hardship exceptions to this deadline.

Do I need a qualified intermediary, or can my attorney handle it?

You need a QI. The IRS prohibits your attorney, CPA, real estate agent, or any person who has acted as your agent within the past two years from serving as your intermediary. An independent, third-party QI is required.

Are 1031 exchanges still allowed after the 2025 tax law changes?

Yes. The "One Big Beautiful Bill" signed on July 4, 2025 preserved Section 1031 without modification. All exchange types remain fully qualifying, and there are no new dollar caps or phase-outs.

Can I exchange my rental property for property in a different state?

Yes. IRC Section 1031 permits exchanges of real property located anywhere in the United States. Cross-state exchanges are common and fully compliant.

Start Your Exchange Today

If you are planning to sell a rental property, the time to engage your qualified intermediary is now, not at closing. Granite Exchange Services has guided investors through over 20,000 exchanges since 2000, safeguarding more than $1 billion in client funds. As an independent, CES-certified QI, we give you direct access to a dedicated exchange counselor who knows your transaction from start to finish. No call centers. No handoffs. Call 800-899-6959 or start your exchange online to lock in your tax deferral before your next closing date.