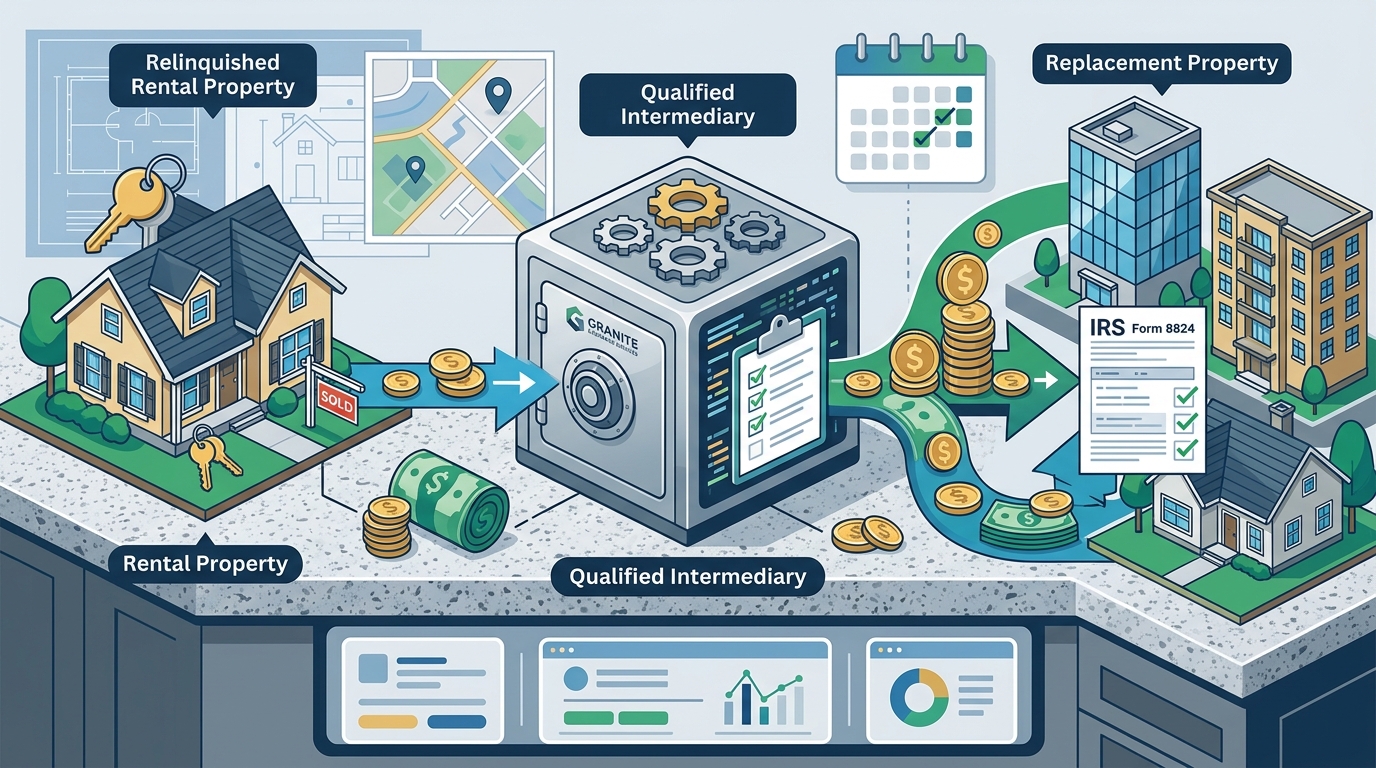

Selling a rental property can trigger a combined federal and state tax bill that exceeds 30% of your gain. A 1031 exchange is a tax-deferral strategy authorized under IRC Section 1031 that lets you reinvest your full sale proceeds into another investment property and defer capital gains taxes, depreciation recapture, and the 3.8% net investment income tax. Whether you own a single rental house or a portfolio of apartment buildings, this guide walks you through every step of the process, from engaging a qualified intermediary to closing on your replacement property and filing Form 8824.

What Is a 1031 Exchange?

A 1031 exchange is a transaction that allows a real estate investor to sell an investment property and defer capital gains taxes by reinvesting the proceeds into another like-kind property. The term "like-kind" refers to the nature or character of the property, not its grade or quality. That means you can exchange a single-family rental for an apartment complex, a commercial warehouse, or even a Delaware Statutory Trust (DST) interest.

A qualified intermediary (QI) is an independent third party that holds the sale proceeds and facilitates the exchange documentation so the investor never takes constructive receipt of the funds. If the money touches your bank account at any point, the exchange fails.

Does Your Rental Property Qualify?

To qualify for a 1031 exchange, both the property you sell (the relinquished property) and the property you buy (the replacement property) must be held for investment or productive use in a trade or business. Rental properties, whether residential or commercial, are among the most common assets exchanged under Section 1031.

Properties That Qualify

- Single-family rental homes

- Multifamily apartment buildings

- Commercial office, retail, and industrial properties

- Vacant land held for investment

- Mixed-use buildings

Properties That Do Not Qualify

- Primary residences

- Vacation homes used exclusively for personal purposes

- Fix-and-flip inventory held primarily for resale

- Stocks, bonds, or partnership interests

Review the full list of 1031 exchange qualifications before you list your property.

Step-by-Step Process for a Rental Property 1031 Exchange

Step 1: Engage a Qualified Intermediary Before Closing

Your QI must be in place before the sale of your rental property closes. The exchange agreement and assignment documents must be signed and executed before the closing date. A 1031 exchange cannot be established retroactively.

Step 2: Sell Your Rental Property

Close on the sale of your relinquished property. At closing, all net proceeds transfer directly to your qualified intermediary and are deposited into a segregated, FDIC-insured exchange trust account. You never receive the funds.

Step 3: Identify Replacement Property Within 45 Days

You have exactly 45 calendar days from the closing date to identify potential replacement properties in writing to your QI. The IRS allows you to identify up to three properties regardless of value under the 3-property rule, or more properties under the 200% rule.

Step 4: Close on Replacement Property Within 180 Days

You must complete the purchase of one or more identified replacement properties within 180 calendar days of the relinquished property closing. Your QI coordinates the disbursement of exchange funds directly to escrow.

Step 5: Report the Exchange on Form 8824

File IRS Form 8824 with your federal tax return for the year in which the exchange occurred. Your QI provides the documentation you need to complete this form accurately.

Critical Deadlines: The 45-Day and 180-Day Rules

Missing either deadline disqualifies the entire exchange and makes your gain fully taxable. Both timelines are measured in calendar days, not business days, and they run concurrently from the closing date of the relinquished property.

| Deadline | Duration | What Happens |

|---|---|---|

| Identification Period | 45 calendar days | Written identification of replacement properties must be received by your QI by midnight on day 45. |

| Exchange Period | 180 calendar days | Replacement property must close by the earlier of day 180 or the due date (with extensions) of your federal tax return. |

| Tax Return Extension | Varies | If your property closes late in the calendar year, a filing extension may be necessary to preserve the full 180-day window. |

Deadlines falling on weekends or federal holidays advance to the next business day per IRC Section 7503.

Exchange Types for Rental Property Investors

Not every rental property sale follows the same playbook. The right exchange structure depends on your timeline, your market, and your goals.

| Exchange Type | Best For | Key Feature |

|---|---|---|

| Delayed (Forward) Exchange | Most rental property sellers | Sell first, buy within 180 days |

| Reverse Exchange | Competitive markets | Buy replacement before selling |

| Improvement/Build-to-Suit Exchange | Value-add investors | Use proceeds for construction on replacement property |

| DST Exchange | Passive income seekers | Fractional ownership in institutional real estate |

A Delaware Statutory Trust (DST) is a legal entity that holds title to institutional-grade real estate and issues fractional beneficial interests that qualify as like-kind property under Rev. Rul. 2004-86. DSTs are popular among rental property owners ready to exit active management while continuing to defer taxes.

How to Avoid Taxable Boot

Boot is any non-like-kind value received in an exchange, typically cash proceeds you keep or a reduction in mortgage debt. Boot is taxable in the year it is received. To defer 100% of your capital gain, follow two rules:

- Reinvest all net proceeds from the sale into the replacement property.

- Acquire property of equal or greater value with equal or greater debt.

Learn more about how boot works and how to minimize it.

Key Takeaways

- A rental property held for investment qualifies for a 1031 exchange under IRC Section 1031.

- Your qualified intermediary must be engaged before the relinquished property closes.

- You have 45 calendar days to identify and 180 calendar days to close on replacement property.

- All exchange proceeds must go directly to your QI and never pass through your accounts.

- To defer 100% of the gain, reinvest all proceeds and match or exceed the relinquished property's value and debt.

- Section 1031 was preserved fully intact under the 2025 tax law signed July 4, 2025.

- An independent, CES-certified QI like Granite Exchange Services provides hands-on guidance through every step.

Frequently Asked Questions

Can I do a 1031 exchange on a single rental property?

Yes. There is no minimum number of properties or dollar amount required. A single rental house qualifies as long as it is held for investment or business use.

Can I exchange my rental property for a different type of real estate?

Yes. Like-kind is broadly defined for real estate. You can exchange a rental house for a commercial building, vacant land, an apartment complex, or a DST interest.

What happens if I miss the 45-day identification deadline?

The exchange fails entirely. Your sale proceeds become taxable, and you will owe capital gains tax, depreciation recapture, and potentially the 3.8% net investment income tax on the gain.

Do I need a qualified intermediary?

Yes. The IRS requires that a neutral third party hold the exchange funds. If the proceeds hit your bank account even briefly, the exchange is disqualified.

Can I exchange a rental property in one state for property in another?

Absolutely. IRC Section 1031 permits exchanges of real property located anywhere in the United States. Cross-state exchanges are common.

Was the 1031 exchange changed by the 2025 tax law?

No. The "One Big Beautiful Bill" signed on July 4, 2025 left Section 1031 fully intact with no new caps, phase-outs, or restrictions.

How much tax can I defer with a 1031 exchange on a rental property?

Federal long-term capital gains rates of 15 to 20%, the 3.8% net investment income tax, and 25% depreciation recapture can combine to exceed 28% of your gain before state taxes. A 1031 exchange defers all of it.

Can I convert my primary residence into a rental and then do a 1031 exchange?

Potentially. If you convert your home to a rental and hold it for investment purposes for a sufficient period, it may qualify. Consult a tax advisor to ensure compliance with IRS guidelines.

Start Your 1031 Exchange Today

Granite Exchange Services has guided investors through over 20,000 exchanges since 2000. As an independent, CES-certified qualified intermediary, we provide one dedicated counselor, direct phone access, FDIC-insured segregated accounts, and hands-on guidance from your first call through final closing. No call centers. No corporate runarounds.

Contact Granite Exchange Services or call 800-899-6959 to speak with a CES-certified exchange specialist today.